Abstract

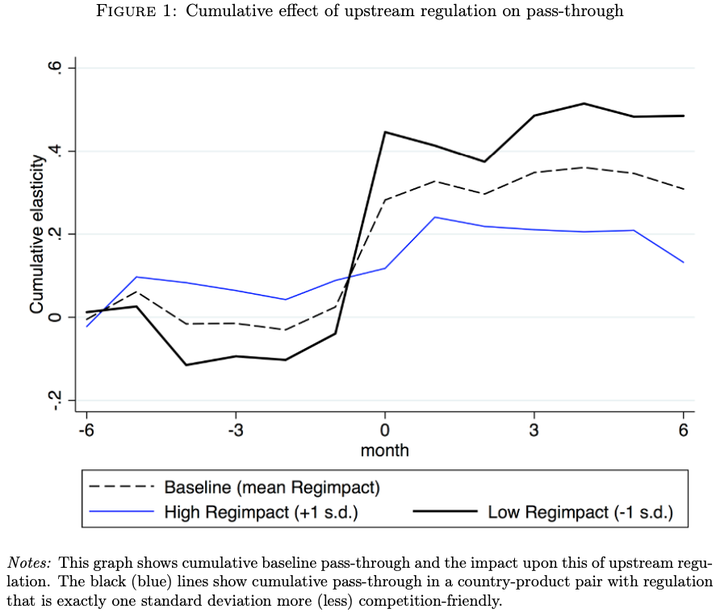

We examine whether value-added tax pass-through depends on market structure. We extend existing theory to characterize the roles of imperfect competition and product differentiation, then investigate these relationships empirically using a panel of 14 Eurozone countries between 1999 and 2013. Relative to baseline total pass-through of up to 33 percent, we estimate that a one-standard-deviation rise in the competition-friendliness of regulation in upstream markets increases pass-through by up to 22 percentage points, and an equivalent rise in the scope for quality differentiation increases pass-through by up to 38 percentage points.

Type

Publication

National Tax Journal